When a loss happens, whether it is a storm, a fire, or a fallen tree, most people expect their insurance to help them rebuild and move forward. What many people do not realize is that how much a policy pays after a claim often depends on one important detail that is easy to overlook until it matters most. That detail is how the value of damaged property is calculated. Two common terms you will see in insurance policies are Replacement Cost and Actual Cash Value. While they sound similar, they can lead to very different outcomes after a loss.

Understanding the difference ahead of time can help you avoid surprises and make coverage decisions that better match your expectations.

What Is Replacement Cost Coverage?

What Is Replacement Cost Coverage?

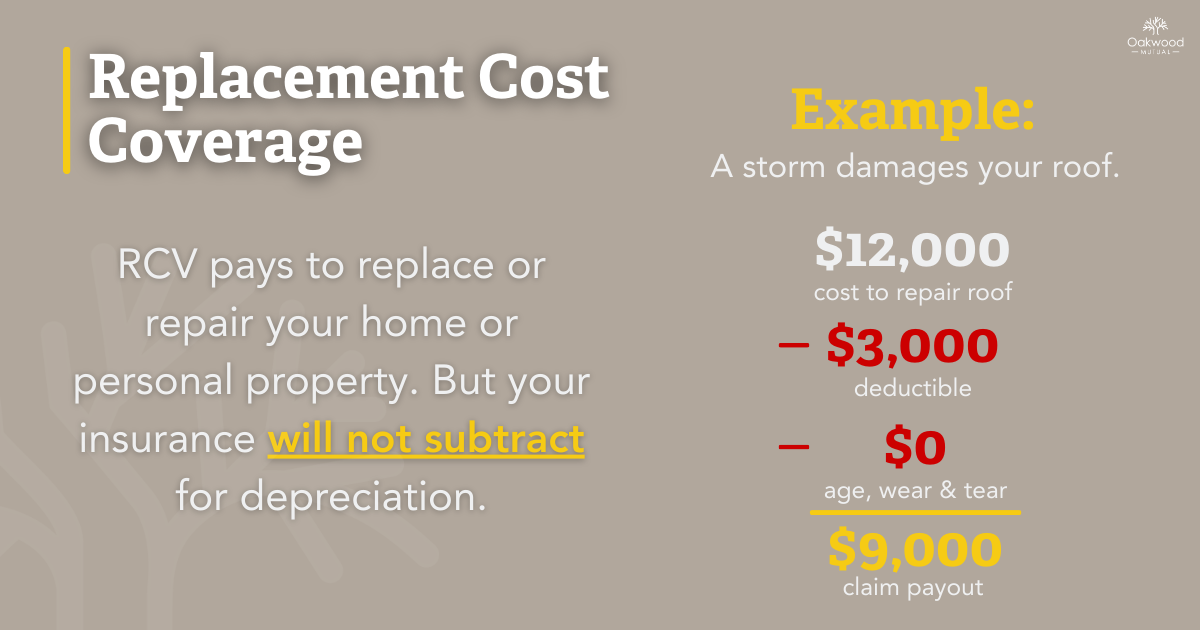

Replacement Cost coverage pays what it costs to repair or replace damaged property with materials of similar kind and quality. It does not deduct for age or wear and tear.

In simple terms, Replacement Cost focuses on what it would cost to replace the property today, not what it was worth just before it was damaged.

How Replacement Cost Works

Imagine a windstorm damages your roof. Even if that roof is several years old, Replacement Cost coverage is designed to help pay for a new roof using comparable materials at current prices.

Benefits of Replacement Cost Coverage

Replacement Cost coverage can provide several advantages, especially for primary homes and essential structures.

It helps restore property closer to its condition before the loss. It reduces out-of-pocket expenses after a claim. It offers more predictable claim outcomes. For many homeowners, it provides peace of mind knowing that depreciation will not reduce the payment.

Important Rules to Know

Replacement Cost coverage usually comes with specific conditions.

Coverage limits must be accurate and kept up to date. Repairs or replacement typically must be completed to receive the full payment. Policies may include time limits or documentation requirements. Premiums are generally higher than those for Actual Cash Value coverage.

Replacement Cost coverage is not unlimited. Payments are still subject to the limits and terms of the policy.

What Is Actual Cash Value Coverage?

What Is Actual Cash Value Coverage?

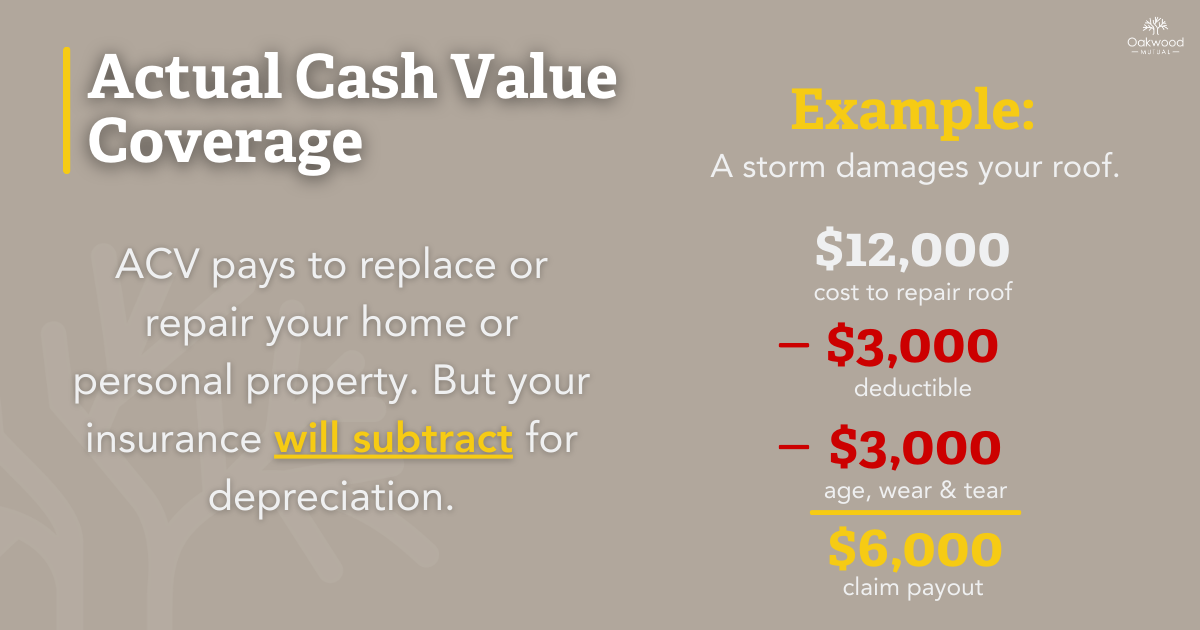

Actual Cash Value, often referred to as ACV, pays the cost to replace damaged property minus depreciation. Depreciation reflects the age, condition, and wear of the property over time.

This means the claim payment is based on what the property was worth right before the loss, not what it would cost to replace it today.

How Actual Cash Value Works

Using the roof example again, if the roof is older and has already experienced wear, an Actual Cash Value claim would reduce the payment to account for that age. Even if the cost to replace the roof today is high, the payout would reflect depreciation.

Benefits of Actual Cash Value Coverage

Actual Cash Value coverage typically has a lower premium cost. It may make sense for older structures, outbuildings, or secondary buildings where full replacement is not expected. For some property owners, the lower upfront cost is a practical choice.

Limitations to Be Aware Of

Depreciation can significantly reduce claim payments. Out-of-pocket costs after a loss are usually higher. Claim payouts can be surprising if policyholders expect full replacement. This type of coverage is less suitable when restoring property is financially important.

Actual Cash Value coverage is not inherently bad, but it works best when expectations are clearly understood.

Replacement Cost vs. Actual Cash Value: A Quick Comparison

The difference between these two coverage options often becomes most noticeable after a claim occurs.

Replacement Cost coverage generally pays more after a loss, minimizes out-of-pocket expenses, and costs more upfront in premiums.

Actual Cash Value coverage usually has lower premiums but results in lower claim payments and requires greater financial responsibility after a loss.

Neither option is right for everyone. The best choice depends on the property, the budget, and personal expectations.

What Determines Which Coverage You Have?

Several factors influence whether property is insured at Replacement Cost or Actual Cash Value.

These factors include the type of structure, such as a home, barn, or outbuilding, the age and condition of the property, how the property is used, policy endorsements that have been selected, and underwriting guidelines.

In many cases, different structures on the same policy may be valued in different ways.

How to Decide What Is Right for You

How to Decide What Is Right for You

Choosing between Replacement Cost and Actual Cash Value comes down to practical questions.

Could you afford to replace the property out of pocket? Is full restoration important to you? How old is the structure or item being insured? Would a reduced claim payment create financial strain?

There is no one-size-fits-all answer, but there is value in reviewing coverage periodically as circumstances change.

Why Your Local Agent Matters

Insurance language can be confusing, especially for people who have never experienced a loss. A local agent helps translate policy terms into real-world expectations and helps ensure coverage aligns with what matters most to you.

These conversations are best had before something happens, not after.

Replacement Cost and Actual Cash Value are two different ways of valuing property after a loss. One focuses on today’s cost to replace the property. The other accounts for age and depreciation.

Neither option is automatically right or wrong. Understanding the difference allows you to make informed decisions and avoid surprises when it matters most.